阿摩線上測驗

阿摩線上測驗

題組內容

3. International Appliance Company is a diversified corporation with separate and

distinct operating divisions. Each division’s performance is evaluated on the basis of total

dollar profits and return on division investment.

The Fridge Division manufactures and sells refrigerators. The Division expected to sell

15,000 units in the coming year, with selling price budgeted at $400 per unit. Fridge’s

division manager believes sales can be increased if sales price is reduced. A market research

study conducted by an independent firm indicates that a 5% reduction in the sales price ($20)

will increase sales volume to 17,500 units. Fridge has sufficient production capacity to

manage this increased volume with no increase in fixed cost. At the present time, Fridge uses

a compressor in its refrigerators, which it purchases from an outside supplier at a cost of $70

each.

The company has another division, the Compressor Division, which currently

manufactures a compressor that is similar to the one used by the Fridge and sells it

exclusively to outside firms. The division manager of Fridge has approached the manager of

the Compressor Division, proposing to buy compressors from the Compressor Division. The

manager of Fridge wants all compressors it uses to come from one supplier and has offered to

pay $50 for each compressor. Specifications for the Fridge compressor are slightly different.

They would reduce the Compressor Division’s raw materials cost by $2 per unit. In addition,

the Compressor Division would not incur any variable marketing cost for the unit sold to

Fridge.

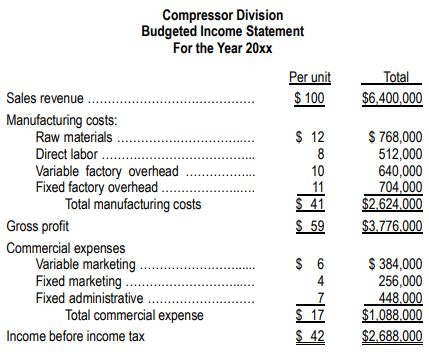

The Compressor Division has the capacity to produce 75,000 units. The coming year’s

budgeted income statement for the Compressor Division shown below is based on a sales

volume of 64,000 units, without considering Fridge’s proposal.

Required:(須列出計算過程,計算至整數位)

distinct operating divisions. Each division’s performance is evaluated on the basis of total

dollar profits and return on division investment.

The Fridge Division manufactures and sells refrigerators. The Division expected to sell

15,000 units in the coming year, with selling price budgeted at $400 per unit. Fridge’s

division manager believes sales can be increased if sales price is reduced. A market research

study conducted by an independent firm indicates that a 5% reduction in the sales price ($20)

will increase sales volume to 17,500 units. Fridge has sufficient production capacity to

manage this increased volume with no increase in fixed cost. At the present time, Fridge uses

a compressor in its refrigerators, which it purchases from an outside supplier at a cost of $70

each.

The company has another division, the Compressor Division, which currently

manufactures a compressor that is similar to the one used by the Fridge and sells it

exclusively to outside firms. The division manager of Fridge has approached the manager of

the Compressor Division, proposing to buy compressors from the Compressor Division. The

manager of Fridge wants all compressors it uses to come from one supplier and has offered to

pay $50 for each compressor. Specifications for the Fridge compressor are slightly different.

They would reduce the Compressor Division’s raw materials cost by $2 per unit. In addition,

the Compressor Division would not incur any variable marketing cost for the unit sold to

Fridge.

The Compressor Division has the capacity to produce 75,000 units. The coming year’s

budgeted income statement for the Compressor Division shown below is based on a sales

volume of 64,000 units, without considering Fridge’s proposal.

Required:(須列出計算過程,計算至整數位)