阿摩線上測驗

阿摩線上測驗

題組內容

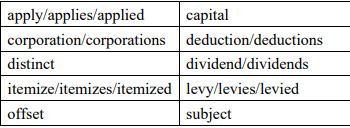

III. Word choice: Pick from the following words to fill in the blanks from (a) to (j)

THE BASIC STRUCTURE OF THE FLAT TAX

The flat tax. The flat tax distinguishes between income from labor and “income” from business. There is no tax on (g) income, e.g., (i) , interest, and (g) gains, per se.

Labor income of individuals in excess of personal exemptions and a standard (a) is (h) to a flat rate of tax. There are no (b) (a) for personal expenditures of individual taxpayers.

The same tax rate is (f) to business income as to the income of individuals. The tax on business

income is (d) without regard to organizational form; that is, it (f) equally to the income of proprietorships, partnerships, and (j) .

The two taxes, on labor income and on business income, are totally (e) . Business losses cannot be

used to (c) labor income, and personal exemptions and the standard (a) can be used only

to (c) labor income; they cannot be used to reduce tax on business income. In the parlance of tax

professionals, the flat tax consists of two “schedular” taxes.

The income tax. By comparison, the U.S. income tax on individuals is a “global” income tax; income from business and income from (g) (including interest and (i) ) are lumped together with

labor income, as are net (g) gains (which, however, are (h) to a maximum rate less

than the top marginal rate (f) to ordinary income). Thus, business losses (and, within limits, net

(g) losses and investment expenses) can be (c) against aggregate income from other sources.

Unlike the flat tax, there are (b) (a) for medical expenses, state and local taxes,

mortgage interest related to owner-occupied housing, charitable contributions, and employee expenses (in excess of two per cent of adjusted gross income). These reduce global income, as do personal exemptions and the standard (a) , which is an alternative to (b) (a) .

Business income under the income tax. The treatment of business income under the U.S. income tax is very different from that under the flat tax. Neither proprietorships nor partnerships, per se, pay income tax. Rather, proprietors include net business income in their tax base and partners include their shares of income or losses of partnerships. (j) are taxed as legal entities apart from their owners, except in the case of certain closely held (j) (S (j) ); thus, corporate losses generally cannot be used to (c) income from other sources. Individuals pay tax on (i) , with no relief for corporate taxation

of the income giving rise to (i) .

The flat tax. The flat tax distinguishes between income from labor and “income” from business. There is no tax on (g) income, e.g., (i) , interest, and (g) gains, per se.

Labor income of individuals in excess of personal exemptions and a standard (a) is (h) to a flat rate of tax. There are no (b) (a) for personal expenditures of individual taxpayers.

The same tax rate is (f) to business income as to the income of individuals. The tax on business

income is (d) without regard to organizational form; that is, it (f) equally to the income of proprietorships, partnerships, and (j) .

The two taxes, on labor income and on business income, are totally (e) . Business losses cannot be

used to (c) labor income, and personal exemptions and the standard (a) can be used only

to (c) labor income; they cannot be used to reduce tax on business income. In the parlance of tax

professionals, the flat tax consists of two “schedular” taxes.

The income tax. By comparison, the U.S. income tax on individuals is a “global” income tax; income from business and income from (g) (including interest and (i) ) are lumped together with

labor income, as are net (g) gains (which, however, are (h) to a maximum rate less

than the top marginal rate (f) to ordinary income). Thus, business losses (and, within limits, net

(g) losses and investment expenses) can be (c) against aggregate income from other sources.

Unlike the flat tax, there are (b) (a) for medical expenses, state and local taxes,

mortgage interest related to owner-occupied housing, charitable contributions, and employee expenses (in excess of two per cent of adjusted gross income). These reduce global income, as do personal exemptions and the standard (a) , which is an alternative to (b) (a) .

Business income under the income tax. The treatment of business income under the U.S. income tax is very different from that under the flat tax. Neither proprietorships nor partnerships, per se, pay income tax. Rather, proprietors include net business income in their tax base and partners include their shares of income or losses of partnerships. (j) are taxed as legal entities apart from their owners, except in the case of certain closely held (j) (S (j) ); thus, corporate losses generally cannot be used to (c) income from other sources. Individuals pay tax on (i) , with no relief for corporate taxation

of the income giving rise to (i) .