阿摩線上測驗

阿摩線上測驗

題組內容

6. (35%) Let wT denote the terminal wealth of a uni-dollar investment after T periods. Consider two possible cumulative distribution functions (CDFs) for wT as follows. where N(μ, σ2) represents the normal distribution with the mean to be u and the variance to be σ2. For any utility function U'(•) ≥ 0, the expected utility under F or G is

where N(μ, σ2) represents the normal distribution with the mean to be u and the variance to be σ2. For any utility function U'(•) ≥ 0, the expected utility under F or G is

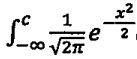

dx is the CDF for the standard normal distribution. where M is a positive constant, and the expected utility under F is

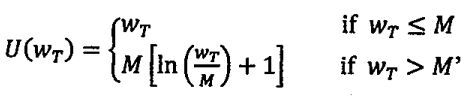

dx is the CDF for the standard normal distribution. where M is a positive constant, and the expected utility under F is6.3 (20%) Consider a utility function

where M is a positive constant, and the expected utility under F is

6.3.2 (10%) If II can be expressed as M[aΦ(β) + γe-δ2/2], what are a, β,γ, and δ?