活動名稱

【解題達人! We want you!】

活動說明

阿摩站上可謂臥虎藏龍,阿摩發出200萬顆鑽石號召達人們來解題!

針對一些題目可能有疑問但卻缺少討論,阿摩主動幫大家尋找最佳解!

懸賞試題多達20萬題,快看看是否有自己拿手的科目試題,一旦你的回應被選為最佳解,一題即可獲得10顆鑽石。

懸賞時間結束後,只要摩友觀看你的詳解,每次也會得到10顆鑽石喔!

關於鑽石

如何使用:

- ✔懸賞試題詳解

- ✔購買私人筆記

- ✔購買懸賞詳解

- ✔兌換VIP

(1000顆鑽石可換30天VIP) - ✔兌換現金

(50000顆鑽石可換NT$4,000)

如何獲得:

- ✔解答懸賞題目並被選為最佳解

- ✔撰寫私人筆記販售

- ✔撰寫詳解販售(必須超過10讚)

- ✔直接購買 (至站內商城選購)

** 所有鑽石收入,都會有10%的手續費用

近期考題

【非選題】

【題組】(三) 有一直徑為 40 mm 的均質圓軸,承受 20 N‧m 的扭矩, 以 300 rpm 的轉速旋轉,試求軸之切線速度(單位:m/s) 與傳輸的功率(單位:瓦特)為多少? (9 分)

二、 試回答以下機械設計相關問題:(本題共 25 分)

【題組】(三) 有一直徑為 40 mm 的均質圓軸,承受 20 N‧m 的扭矩, 以 300 rpm 的轉速旋轉,試求軸之切線速度(單位:m/s) 與傳輸的功率(單位:瓦特)為多少? (9 分)

【非選題】

【題組】

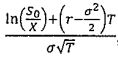

8. (30%) Consider a power call or put option with the payoff at the maturity T as

respectively, where St is the stock price at time t, i is a positive-integer exponent, and Xi denotes the

strike price. Under the Black-Scholes framework, their respective value functions today (t = 0) are

where

, r is the risk-free interest rate, o is the stock price volatility, and N(•) is the cumulative OVF

distribution function of the standard normal distribution defined as

, r is the risk-free interest rate, o is the stock price volatility, and N(•) is the cumulative OVF

distribution function of the standard normal distribution defined as

where n(•) is the probability density function of the standard normal distribution.

【題組】

(d)(4%) In what condition does