阿摩線上測驗

阿摩線上測驗

題組內容

8. (30%) Consider a power call or put option with the payoff at the maturity T as

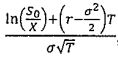

respectively, where St is the stock price at time t, i is a positive-integer exponent, and Xi denotes the strike price. Under the Black-Scholes framework, their respective value functions today (t = 0) are

where

, r is the risk-free interest rate, o is the stock price volatility, and N(•) is the cumulative OVF distribution function of the standard normal distribution defined as

, r is the risk-free interest rate, o is the stock price volatility, and N(•) is the cumulative OVF distribution function of the standard normal distribution defined as

where n(•) is the probability density function of the standard normal distribution.

(d)(4%) In what condition does